The AI Dollar Thesis

From Petrodollars to AI Dollars: The Geopolitics of a New Economic Order

As artificial intelligence becomes the engine of global productivity, a new thesis is quietly emerging: the rise of the "AI dollar." Much like the petrodollar system, which underpinned U.S. dominance in the second half of the 20th century, the AI dollar would revolve around the idea that nations across the globe earn and spend U.S. dollars in exchange for AI infrastructure, IP, and services that are controlled primarily by American firms. But how plausible is this scenario—and what would it take for it to become a systemic reality?

The Petrodollar Blueprint

The petrodollar system emerged in the 1970s when the U.S. negotiated with oil-producing nations to price oil exclusively in U.S. dollars. This arrangement forced countries around the world to hold dollars to participate in the global energy market, reinforcing the dollar as the world’s reserve currency. Even adversaries like Iran and the Soviet Union had to transact in dollars to access oil markets or convert revenues.

This structure offered the U.S. unprecedented monetary leverage, allowing it to run persistent deficits and enforce sanctions that could freeze adversaries out of global markets. The key was that oil was non-negotiable—it powered everything.

Enter the AI Dollar

Fast forward to today. AI is quickly becoming the new critical infrastructure—powering everything from logistics and finance to defense and scientific discovery. The U.S. currently dominates the AI stack:

90% of the world’s most valuable AI companies are headquartered in the U.S., including OpenAI, Anthropic, Google DeepMind, and NVIDIA (CB Insights, 2024).

Nearly all top-tier AI models and cloud infrastructure (e.g., Azure OpenAI, AWS Bedrock) are owned and operated by U.S. firms.

Over 75% of global AI venture capital funding flows through U.S.-based entities (PitchBook, 2023).

Foreign governments, enterprises, and startups are already subscribing to U.S.-built AI services, priced and transacted in dollars. Simultaneously, countries like India, Vietnam, and Kenya are supplying labeled data, chip manufacturing, and contractor labor—often paid in USD. This sets up a potential AI economic loop:

Supply-side actors get paid in dollars, only to spend those same dollars to access U.S. AI capabilities.

This is the backbone of what some are calling the "AI dollar system"—a digital mirror of the old petrodollar arrangement.

How the AI Dollar Could Take Off

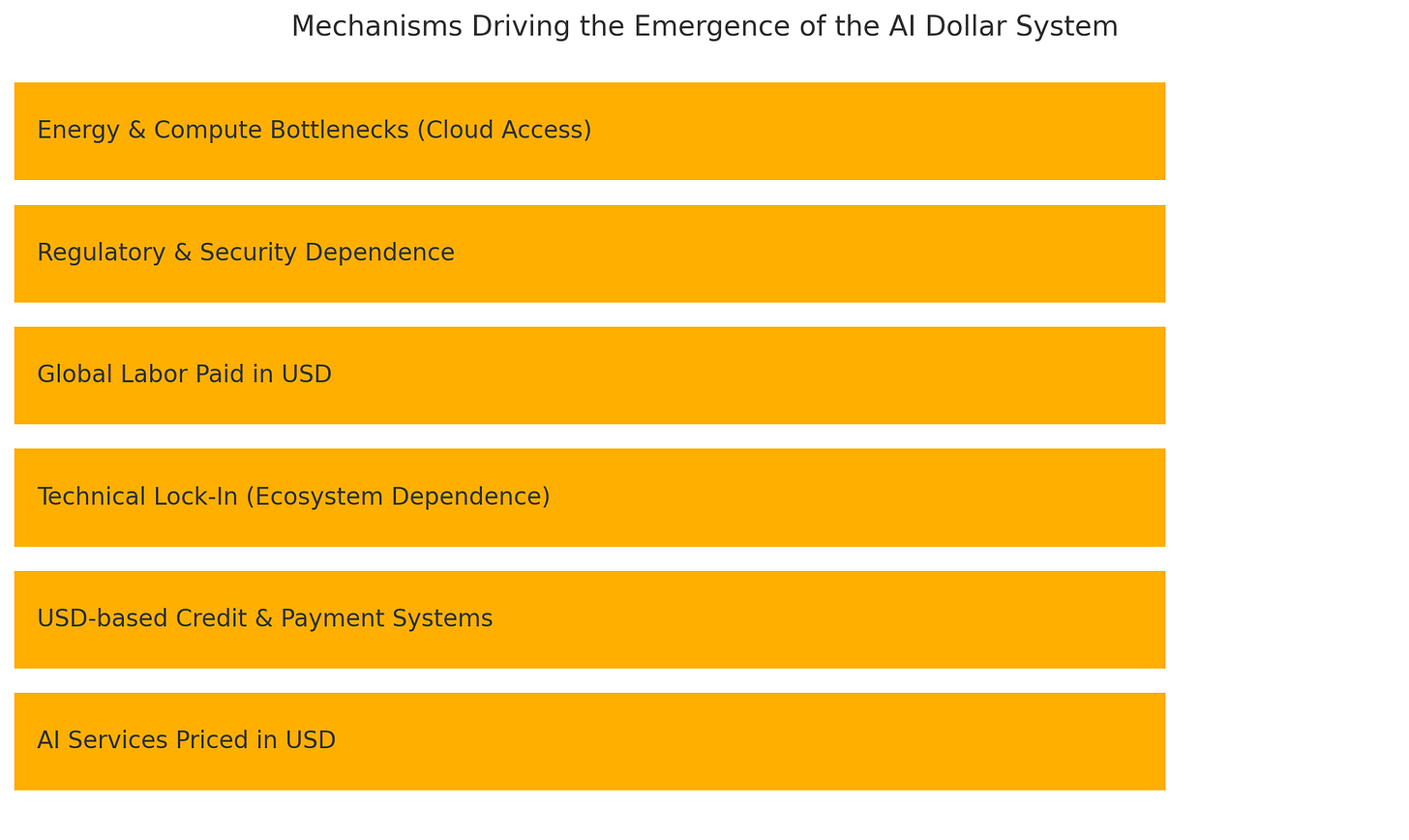

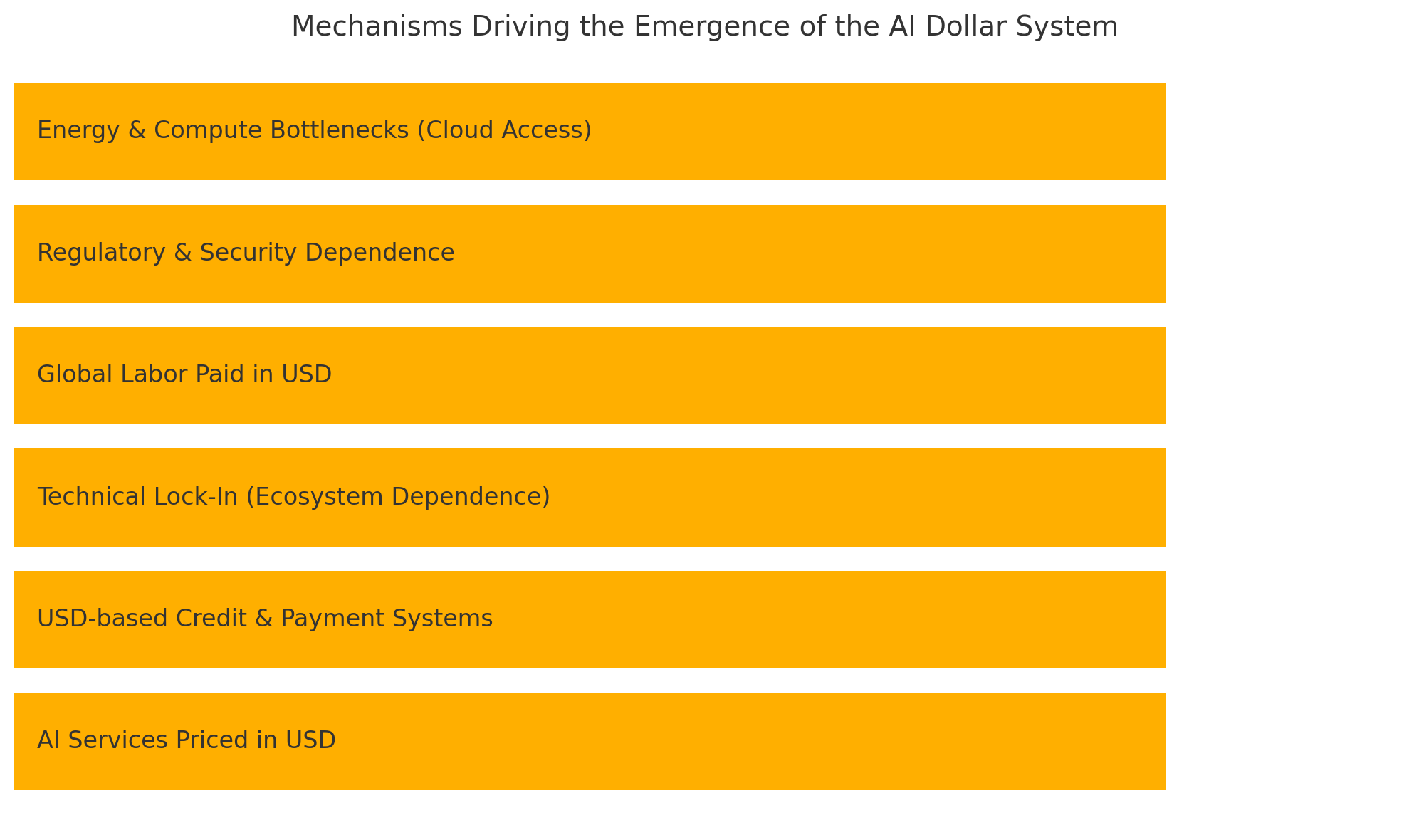

For the AI dollar system to solidify, several reinforcing mechanisms would need to align:

Pricing Standardization: AI services, training, inference, and API access across major providers (AWS, Azure, Google) are already priced in USD. As global businesses embed AI into daily operations, recurring AI subscriptions and compute purchases will institutionalize dollar flows.

Credit and Payment Systems: As AI services become mission-critical, firms across emerging and developed markets will seek credit lines, payment gateways, and insurance products denominated in USD, reinforcing the need for dollar liquidity.

Technical Lock-In: Models and APIs will create ecosystem dependencies, making it costly and operationally risky to switch providers. Companies will stick to U.S.-centric AI stacks, paying into them continuously in dollars.

Global Labor Flows: Countries providing data annotation, validation, and custom model training—often located in the Global South—will continue earning USD, tying local economies to the dollar-AI loop.

Regulatory and Security Dependence: Access to advanced AI models for healthcare, national defense, logistics, and financial modeling will become so essential that even adversarial or neutral nations must maintain good standing with U.S. providers, effectively reinforcing dollar-centric contracts and agreements.

Energy and Compute Bottlenecks: Given the chronic underdevelopment of energy infrastructure in much of the Global South, most nations will be unable to independently host large-scale AI workloads. Instead, they will rent compute access from U.S.-based or U.S.-aligned hyperscalers, settling transactions in dollars.

These dynamics together create a feedback loop: the more entrenched AI becomes in global production and governance, the more the dollar remains the medium of exchange for accessing its benefits.

The Invisible Driver: U.S. Entrepreneurial Culture

Beyond infrastructure and capital, there's a subtler force reinforcing U.S. dominance: the global adoption of American entrepreneurial norms. From Silicon Valley's risk-taking ethos to the ubiquity of YC-style product-market fit obsession, the U.S. startup model has become the default operating system for innovation worldwide.

Founders from Nairobi to Tel Aviv to Jakarta are trained on U.S.-built tools, pitch in English, raise in USD, and scale on platforms like AWS and OpenAI. The culture of building with U.S. APIs and integrating into its software stack drives natural demand for its products. And crucially, it embeds U.S. technologies—and the dollar—deep into global workflows before any formal agreements are even made.

This cultural export is not trivial. It's one of the reasons why U.S. tools become the first choice, even when cheaper or locally developed alternatives exist. Like the petrodollar system, the AI dollar may be sustained not only through dominance, but through embeddedness.

Can It Hold?

However, unlike oil, AI isn’t a naturally scarce resource—it can be open-sourced, replicated, and decentralized. Several factors may block the rise of an AI dollar-dominated world:

China’s Parallel Stack: Through the Digital Silk Road and massive subsidies, China is building a full-stack alternative: chips (SMIC), cloud (Baidu, Alibaba), and models (DeepSeek, WuDao). In 2024, DeepSeek overtook ChatGPT as the most downloaded free app globally.

European Regulation: The EU’s AI Act imposes sovereignty-preserving frameworks that discourage full reliance on U.S. platforms. The bloc is pushing for data localization, regulatory audits, and open-source initiatives.

Global South Resistance: Countries in Africa and Latin America increasingly resist being relegated to data labor. Nations like Brazil and Nigeria are investing in local model development and partnering with UAE and India to create non-dollar AI networks.

Rise of Open Source: Tools like Mistral, LLaMA, and Falcon are lowering the barrier to entry for AI sovereignty. Countries or companies can now fine-tune base models and avoid dollar-based platforms altogether.

Why the AI Dollar Could Still Prevail

One overlooked factor reinforcing the AI dollar thesis is the severe infrastructure gap in energy and compute resources across much of the Global South. According to the International Energy Agency (IEA, 2023), over 770 million people still lack access to reliable electricity, and grid instability remains a major issue across Africa, South Asia, and parts of Latin America. Meanwhile, AI workloads require high-density, reliable power supplies and advanced data centers, which are overwhelmingly concentrated in North America and parts of Europe.

Even if emerging markets develop their own models, running them at scale requires massive compute and stable infrastructure—both of which remain largely inaccessible. This means that countries will continue to depend on cloud-based AI access from U.S. providers (AWS, Azure, Google Cloud) and will likely pay for these services in dollars.

In effect, the lack of energy and compute infrastructure abroad creates a bottleneck that reinforces U.S. platform dominance—just as lack of oil production capacity once ensured reliance on OPEC and the petrodollar system.

Strategic Implications for Investors

Still, if U.S. platforms continue to outpace others in capability, and if compute remains highly concentrated, the AI dollar could become a real economic lever. Investors, PE firms, and hedge funds should monitor:

Who controls the most valuable inference APIs and LLM access?

How is global payment for AI services being structured? Are credits, tokens, or stablecoins being pegged to the dollar?

Where are value chains anchored? If training, hosting, and monetization are all in the U.S., dollar dominance will persist.

Which regions are investing in AI infrastructure vs. remaining dependent on U.S. cloud services?

If access to U.S. AI becomes a must-have rather than a nice-to-have, even adversarial nations may find themselves—again—transacting in the dollar.

Final Take

The AI dollar is not inevitable, but it's increasingly plausible. Like oil in the 20th century, AI in the 21st may become the one asset no country can afford to be without. The nation that controls its platforms may, once again, control the global economic rules. Whether this mirrors the petrodollar’s longevity depends on how centralized—and indispensable—AI truly becomes.

Investors betting on geopolitical outcomes should not underestimate the economic gravity of the AI stack. Follow the flows—of data, compute, capital, and currency—and the new world order may come into focus.