The Great Chain Debate

Corporate Blockchains (Google), Ethereum, and the Struggle for Neutral Settlement

August 2025 brought a striking coincidence: within days, Stripe, Circle, and Google all unveiled plans for their own Layer-1 blockchains (L1s). Stripe’s Tempo, Circle’s Arc, and Google Cloud’s Universal Ledger (GCUL) each promise faster payments, “neutral” infrastructure, and compliance-ready design.

At first glance, this looks like a natural evolution: payments companies going “on-chain.” But the deeper questions are harder: Why do they need their own blockchains at all? Why not just stick with existing IT rails or public networks like Ethereum? And what does this say about the future of money?

The answers illuminate a critical divide between corporate neutrality and protocol neutrality, and show why Ethereum, despite the fanfare around corporate chains, remains the bedrock of the internet of value.

Why Build a Blockchain at All?

Skeptics rightly ask: Stripe and Circle already process trillions through existing rails: Visa, Mastercard, ACH, Fedwire. Google already sells cloud infrastructure. Why would these firms bother with the cost and politics of launching a blockchain?

The short answer is: control of economics, compliance, and UX.

Legacy rails work: until they don’t

ACH and wires settle in batch windows, with dollar caps, and often only during business hours. This is a poor fit for always-on, cross-border commerce.

Card networks impose high fees and absorb huge costs managing chargebacks and “friendly fraud.”

Cross-border flows still hop through correspondent banks, FX desks, and reconciliations, a process the BIS has repeatedly flagged as slow and expensive.

A blockchain ledger promises 24/7 atomic settlement, programmable compliance, and fewer intermediaries. In short, a way to collapse costs and latencies baked into 50-year-old rails.

Owning the base layer = owning the knobs

When a company builds an L1, it doesn’t just process payments; it writes the rules of the game:

Economics: capture fees, reorder transactions (MEV), perhaps issue a native token.

Governance: hard-wire compliance, KYC, sanctions, privacy, directly into the ledger.

Performance: design block times, finality, and fee models around payments, not NFTs or DeFi.

Circle’s Arc illustrates this perfectly: USDC becomes the native gas token, so CFOs can pay fees in dollars rather than volatile crypto assets. Stripe’s Tempo is tuned for merchant payments, while Google’s GCUL pitches itself as “neutral infra” for financial institutions, starting with CME.

For these firms, owning an L1 is a form of vertical integration. Instead of renting blockspace on Ethereum, they pave their own roads.

Corporate Neutrality vs. Protocol Neutrality

Each of these firms markets their L1 as “neutral.” But neutrality has two meanings:

Corporate neutrality: vendor-agnostic positioning. Google’s GCUL is not tied to Stripe or Circle. Circle’s Arc may be open to many PSPs. But the governance still sits with the corporation.

Protocol neutrality: credible neutrality enforced by open consensus and distributed governance. This is what Ethereum offers: rules that no CEO or board can tilt in their favor.

Confusing the two is the loophole. Corporate neutrality is marketing. Protocol neutrality is governance. Only the latter ensures a level playing field for counterparties who don’t want to be beholden to any single firm. As Marc Baumann say “do not confuse distribution with trust”.

Why Not Just Use Ethereum?

If Ethereum already supports billions in stablecoin flows, why not simply build on it, or on Ethereum Layer-2 rollups that inherit its security?

Because for Stripe, Circle, and Google, Ethereum is both an asset and a dependency.

Margins: On Ethereum, they are price-takers. Fees and congestion depend on global demand, not their own priorities.

Governance: They cannot dictate upgrades, censorship rules, or compliance policies.

Control: They cannot guarantee UX (e.g., deterministic fees, instant FX) without owning the consensus layer.

In other words, Ethereum is too neutral. Corporations want sovereignty, their own levers for economics and compliance.

But this comes at a cost: fragmentation. Each corporate L1 becomes a silo. A merchant with Stripe balances, a PSP on Arc, and a custodian on GCUL must juggle bridges, liquidity pools, and reconciliation across three ecosystems. The very friction blockchain was meant to erase re-emerges in corporate form.

Do Corporates See Ethereum as a Threat?

Yes, though more precisely, they see it as an uncomfortable dependency.

Circle has built its brand on Ethereum’s liquidity, but Arc hedges against being just a tenant in someone else’s economy.

Stripe sees Ethereum gas markets as a variable it can’t control, so Tempo offers deterministic costs for merchants.

Google positions GCUL as neutral infra, but “neutral” in the corporate sense, not protocol sense, and implicitly in competition with Ethereum’s role as settlement layer.

Ethereum isn’t displaced here; it’s being routed around not because it’s failing, but because it’s too impartial to be captured.

Why Ethereum Matters

Despite the push for proprietary L1s, Ethereum retains structural advantages that corporates cannot replicate:

Credible Neutrality

Open governance means no single vendor controls the rules. This is what sovereigns, asset managers, and regulators ultimately trust.

Liquidity Gravity

In 2024, Ethereum settled $14.26 trillion in stablecoin value, more than Mastercard and nearly Visa scale. It anchors the deepest pools of liquidity, collateral, and risk management.

Productive Collateral

ETH is not just a token, it is a yield-bearing reserve asset. With staking returns of 3–4%, ETH functions as an “Internet Bond.” Corporates can offer efficiency; Ethereum offers a treasury strategy.

Programmability

Ethereum’s composability enables lending, tokenization, restaking, and AI-secured services. Corporate chains may optimize payments, but they do not anchor the multipurpose economy of the internet.

The Treasury Perspective: ETH as Internet Bond

Recent treasury adoption confirms this trajectory:

Nasdaq-listed firms now hold billions in ETH, with hundreds of millions staked via liquid staking tokens, generating yield as if holding a digital bond.

The SEC clarified staking does not constitute a security if properly structured. The OCC allows banks to run validators. FASB rules now let firms book ETH gains/losses at fair value.

Restaking layers like EigenLayer add new yield streams, turning ETH into the multi-yield security layer for tokenization, oracles, and verifiable AI.

No corporate L1 can offer this. They may process payments, but they cannot provide a neutral, yield-bearing reserve asset that treasuries can hold at scale.

The Historical Analogy: AOL vs. TCP/IP

In the 1990s, AOL, CompuServe, and Prodigy promised sleek, neutral gateways to the internet. They onboarded millions, but their walls became constraints. TCP/IP, the open, credibly neutral protocol, won, because it was the standard no one could capture.

Stripe’s Tempo, Circle’s Arc, and Google’s GCUL look like AOL in 1995: fast, user-friendly, distribution-heavy, but ultimately vendor-controlled. Ethereum is TCP/IP: messy, sometimes congested, but credibly neutral and destined to underpin the global economy.

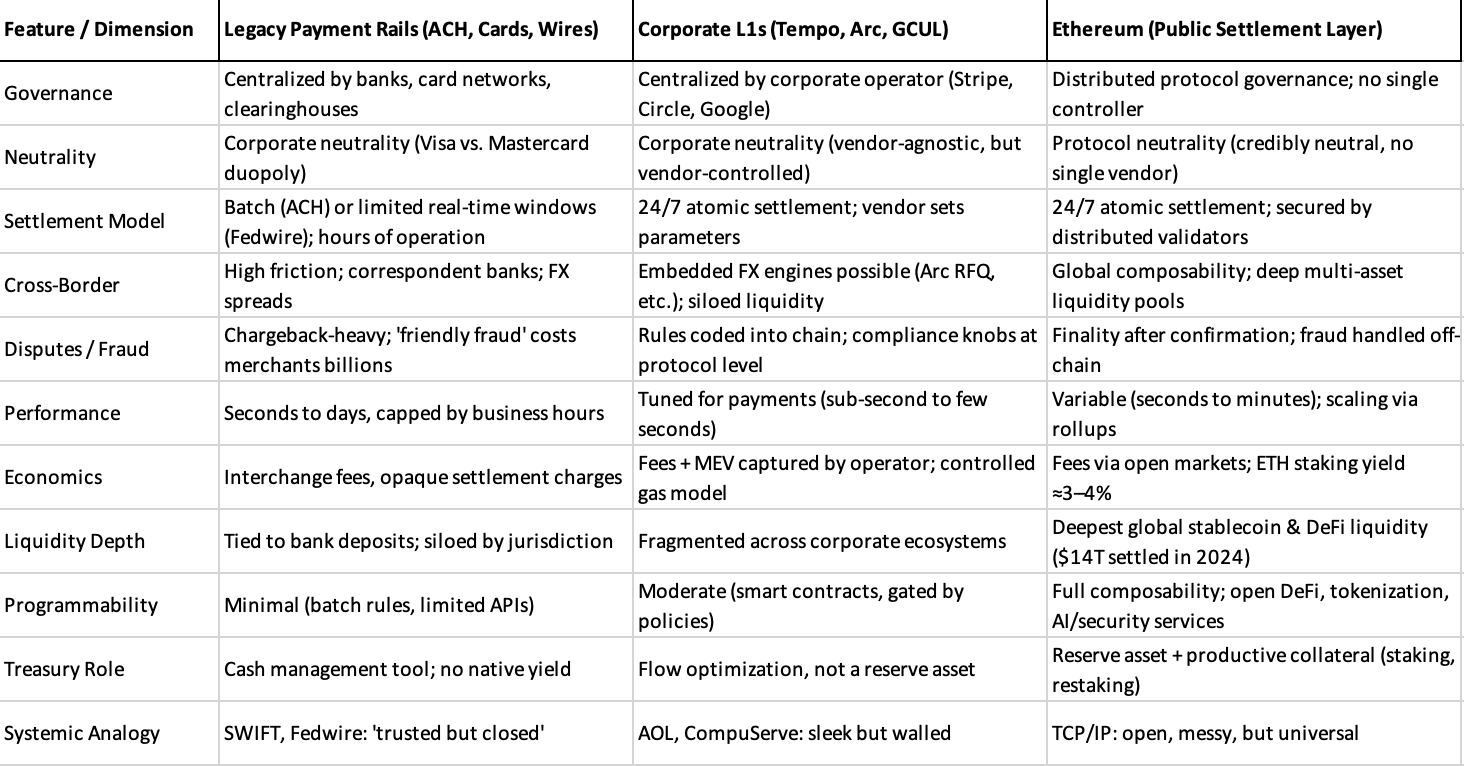

Comparing the rails: Legacy Rails vs. Corporate L1 vs. Ethereum

The Next Five Years: ITS HYBRID, Not Winner-Take-All

The future is not “corporates versus Ethereum,” but corporates plus Ethereum:

Corporate L1s will dominate UX, onboarding, and niche flows, Stripe at the merchant point-of-sale, Circle for USDC-denominated rails, Google for institutional tokenization.

Ethereum will remain the settlement backbone: the liquidity hub, the neutral arbiter, and the Internet Bond for corporate treasuries.

Policy will push for interoperability between corporate L1s and public settlement, standard proofs and audit logs across networks, just as TCP/IP once stitched private networks together.

The great chain debate IS about who owns the rails, and who the world can trust to keep them open.

Corporate L1s may succeed as toll roads. But Ethereum is the highway system, the credibly neutral foundation, the Internet Bond, and the settlement layer of last resort.

Follow us at www.fgnexus.io to own the piece of Ethereum’s Next Decade.

Sources

Circle, Introducing Arc: The USDC-Native Payments Chain (2025).

Fortune, Stripe Building an EVM-Compatible Blockchain (2025).

CME Group & Google Cloud, Universal Ledger Testnet Announcement (2025).

U.S. Congress, GENIUS Act of 2025; Sidley, Latham & Watkins client memos (2025).

ETH Corporate Treasury Playbook, ETH for Corporate Treasuries – August 2025.

NACHA, ACH Settlement Windows; Federal Reserve, Fedwire Hours (2024).

Google “Princeton University Library”. Once there, enter search term “Peter Wayner”. Review Peter’s books! Now answer this question: “Who Invented Bitcoin?”. You see, Poisson Equation is the Intelligent Middle Motor, or the “Satoshi Nakamoto” as it were…

Back in ~2010 when the read/write web was still getting underway, O'Reilly produced a Map of Control, https://cybercultural.com/p/063-the-last-web20-conference-2011/ identifying which firms had staked out which markets. Perhaps this should be updated for web3 (internet of value) and 4.x agentic web which presumes AI. Basically within CashFlow Delta (middle right) you are having a naval arms race, enclaves are forming within Land of Identity and SearchLand is being flooded with slopBots. It would be amusing to predict what might happen in another decade.